The last two decades have seen an explosion of church planting and multiplication ministries and networks. Most church startups are planted by leaders in urban core or inner suburban neighborhoods—and this trend, among others, has financial implications for church planters and their families. But what other factors shape their financial reality?

In a study of 769 planters from across the nation, Barna assessed the general financial condition of church startups and their leaders; how different funding models hamper or facilitate various facets of ministry and family life; and what resources leaders need to effectively manage their personal and church finances. The findings from the full study release today in a new Barna report produced in partnership with Thrivent Financial, Church Startups and Money: The Myths and Realities of Church Planters and Finances.

Here are a few of the standout findings.

Your Leadership Toolkit

Strengthen your message, train your team and grow your church with cultural insights and practical resources, all in one place.

Church Planters Feel Financially Insecure

As part of the survey, Barna asked what Thrivent calls the “5S question,” which has been asked by more than 85,000 people over the past four years. It is a reliable indicator of a person’s perception of their financial situation—their emotions surrounding money, regardless of their actual financial situation. The question is a self-assessment: “Which of the following best describes your current financial situation?”

- Surviving: I require financial assistance to get by.

- Struggling: I am struggling to keep up with day-to-day expenses.

- Stable: I am fairly stable, but just making ends meet.

- Secure: I am fairly secure, able to make ends meet and have some left over.

- Surplus: I have more than I need for myself and my family.

As the graphic shows, church planters’ assessment of their personal financial situation is less stable overall than the general U.S. population. About one-third say they are struggling or surviving (32%), compared to only one in five among all U.S. adults (20%). And they are much less likely to think of their situation as secure (23% vs. 41% of all adults) or in surplus (4% vs. 12%).

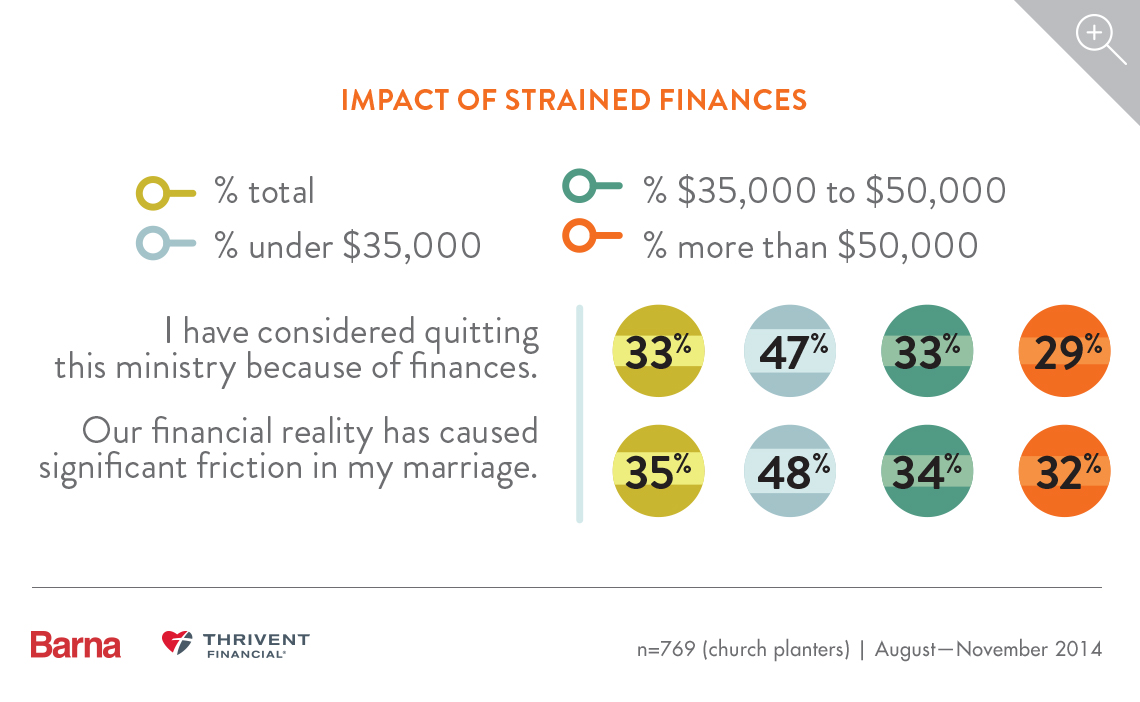

The Impact of Strained Finances

Church planters don’t just feel insecure—many are financially insecure. For the most part, planters’ assessments line up with their strained financial reality. If anything, startup leaders’ perceptions are more positive than one might expect, given that three out of five live on a household income lower than the national average. Thirty-nine percent bring in between $35,000 and $50,000 per year, while one in five reports an annual household income of less than $35,000 (21%). In most states, an income of $31,525 or less qualifies a family for food stamps.

Yet resource constraints take a toll on church planters beyond just financial burdens. One-third of startup leaders admit they have considered quitting ministry because of because of financial strain (33%). This admission, perhaps not surprisingly, is most common among pastors in the lower income bracket (47%). Further, and more worrisome, is the fact that similar proportions of leaders report strains on their marriage as a result of the financial stresses associated with church planting (35%). Again, those in the lower income bracket—and those who assess their personal financial situation as surviving or struggling on the 5S question—are most at risk.

Location Impacts Planters’ Finances

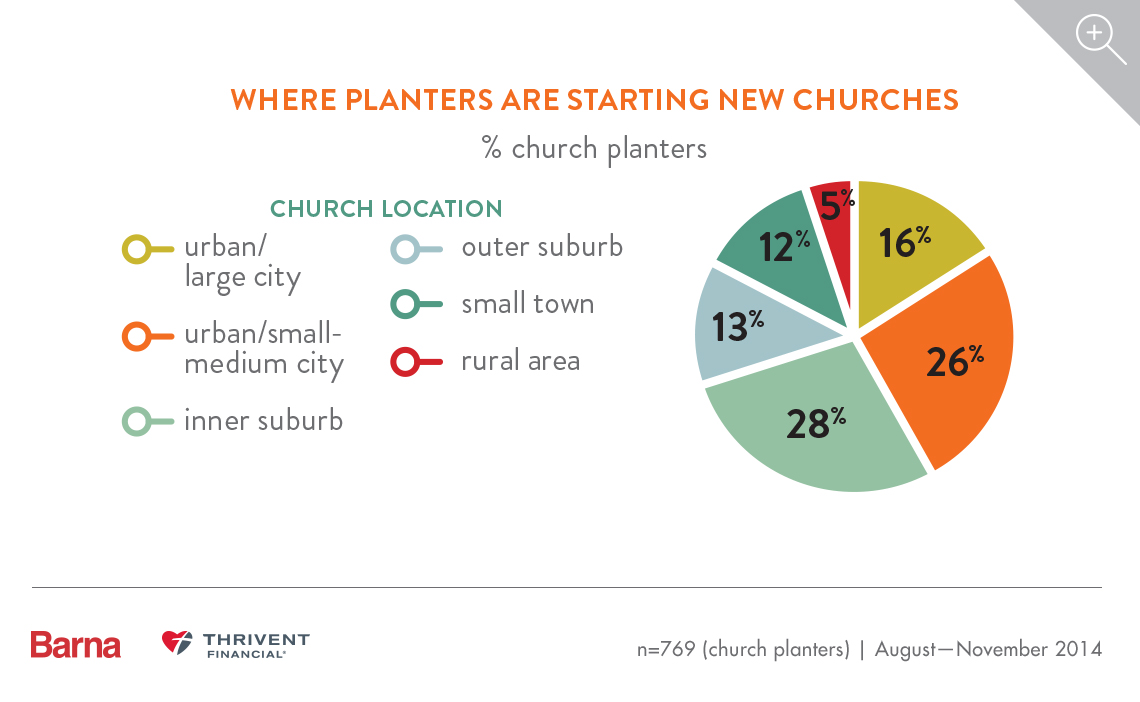

Barna identified several factors that shape the financial reality of today’s church planters, which are explored at length in the new report published today. For instance, church location makes a major impact on startup leaders’ finances. There currently seems to be a concentration of startup efforts in large (16%) and medium (26%) cities and in inner suburbs (28%) that ring major metropolitan areas. Seven out of 10 new churches are in cities or dense inner suburbs.

Ministering in cities presents unique financial challenges for many reasons. Urban centers and their surrounding communities are often diverse, but may be segregated by race, education level, economics, age and cultural differences. Thus, urban planters are more likely to have diverse congregations with varying levels of income and needs, as well as higher operational and facility expenses, than their suburban or rural counterparts. Plus, residents of urban centers, no matter their level of income, live in environments with a higher cost of living. This puts extra strain on a church planter’s personal finances.

Ministering in cities presents unique financial challenges for many reasons. Urban centers and their surrounding communities are often diverse, but may be segregated by race, education level, economics, age and cultural differences. Thus, urban planters are more likely to have diverse congregations with varying levels of income and needs, as well as higher operational and facility expenses, than their suburban or rural counterparts. Plus, residents of urban centers, no matter their level of income, live in environments with a higher cost of living. This puts extra strain on a church planter’s personal finances.

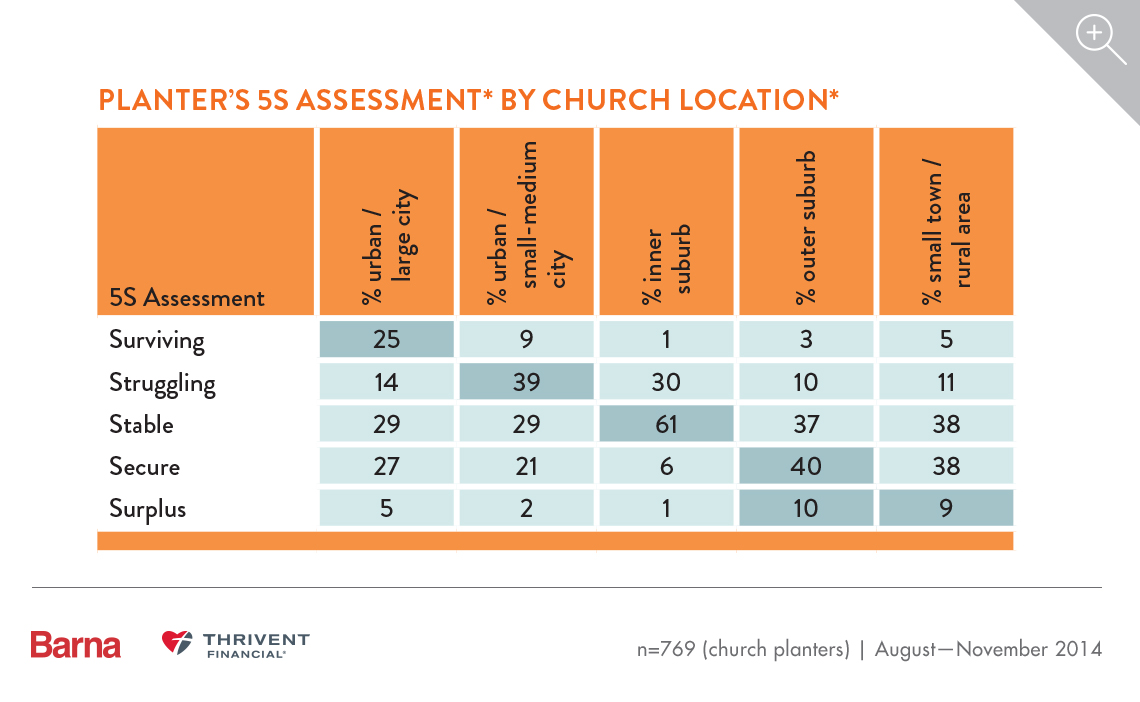

This is reflected in planters’ 5S assessments. Church planters in cities and inner suburbs feel the most financial strain, likely due at least in part to income that insufficiently covers the cost of living in those areas. Also note than planters in outer suburbs, small towns and rural areas more often consider their financial situation above stable.

What the Research Means

“Barna and Thrivent undertook this research to promote healthy conversations about money and ministry,” says Brooke Hempell, vice president of research at Barna Group and director of the study. “We wanted to uncover insights that would be genuinely useful to both church planters and those who support them, reliable data about planters’ financial burdens and the impact of operating with limited resources. In releasing these findings, our hope is to liberate planters to have open and honest conversations about their financial reality—and that those conversations will lead to innovative ideas that advance the church planting movement into a season of unparalleled health and growth.

“Most church planters are entrepreneurial problem solvers,” Hempell continues, “but these findings add up to a daunting reality for even the most resourceful of ministry leaders. The emotional implications are most concerning. Half of church planters with debt say their burden is a significant or even a ‘huge’ problem. One-third have considered quitting ministry because of finances, and 35 percent say financial problems cause friction in their marriage. The latter should be reason for serious reflection. Ministry and marriage are hard enough without the added stress of insufficient support from the Church.

“We see in this data a call to action to denominations and planting networks to provide greater financial support to startup leaders—especially those in urban neighborhoods. If we want planters to engage a community with the gospel, we should free them up financially and administratively to do so. It is not sustainable for the spiritual leaders of new faith communities to live at or below the poverty line or to take on personal debt to cover everyday living expenses. If we believe in the work they are doing, we must commit more financial resources to their success.”

Get your digital copy of “Church Startups and Money” for 30% off using promo code “CHURCHPLANT30”

Comment on this research and follow our work:

Twitter: @davidkinnaman | @roxyleestone | @barnagroup

Facebook: Barna Group

About the Research

The data contained in this report originated through a research study conducted by Barna Group of Ventura, California. The study was commissioned by Thrivent Financial of Minneapolis, Minnesota, and consisted of both qualitative and quantitative methodologies. The 5S Assessment© questions and methodology are copyrighted by Thrivent Financial.

Qualitative research consisted of individual interviews of 20 church planters across the U.S. conducted by Barna researchers via webcam.

The quantitative survey was administered online to leaders of churches (or similar ministries) that self-identified as being in “start-up mode.” A total of 769 church planters participated in the survey, which was conducted August to November 2014. To reach church planters, Barna partnered with planting networks such as Exponential, Converge and Ignite, as well as denominational networks, to send invitations to leaders via these organizations’ normal electronic communication channels. Also invited to participate were members of Barna’s Pastor Panel. The resulting responses were then weighted according to ASARB (Association of Statisticians of American Religious Bodies) statistics on new Protestant church plants between 2010 and 2015 to be nationally representative of regional distribution and denomination.

The vast majority of church planters in this study come from non-mainline denominations (81%), with the largest proportions being on-denominational (15%), Southern Baptist (14%) and undecided/unaffiliated (14%). Nineteen percent of the study’s participants are from mainline denominations (American Baptist, United Church of Christ, Episcopal, Evangelical Lutheran, United Methodist or Presbyterian Church USA).

The sampling error for this study is plus or minus 3.5 percent with a 95-percent confidence interval.

About Barna

Since 1984, Barna Group has conducted more than two million interviews over the course of thousands of studies and has become a go-to source for insights about faith, culture, leadership, vocation and generations. Barna is a private, non-partisan, for-profit organization.

Get Barna in Your Inbox

Subscribe to Barna’s free newsletters for the latest data and insights to navigate today’s most complex issues.